Gas to Graphite

In conversation with the Oakland-based startup closing in on its first commercial plant, rediscovering chemistry we walked away from, and making a methane-pyrolysis bet on breaking China’s lock on battery graphite.

Molten Industries is trying to fix a very specific, very boring‑sounding problem that sits underneath everything from EVs to datacenters: we don’t make our own battery graphite anymore. This is a problem that goes beyond securing the supply chain of American schoolrooms (because, yes, graphite is what’s used in pencils).

Graphite makes up most of the “stuff” in a lithium‑ion battery anode, which means it sits upstream of EVs, robotaxi fleets, grid storage, drones, robots, and the battery systems that increasingly want to be deployed as backup or behind-the-meter solutions for AI datacenters.

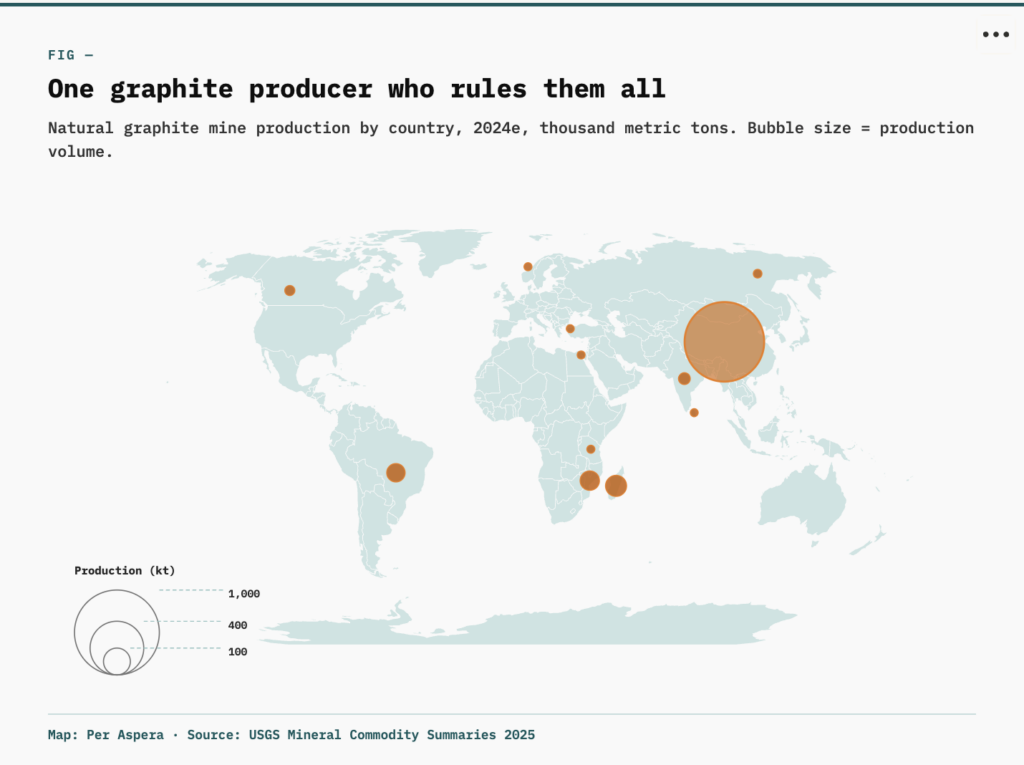

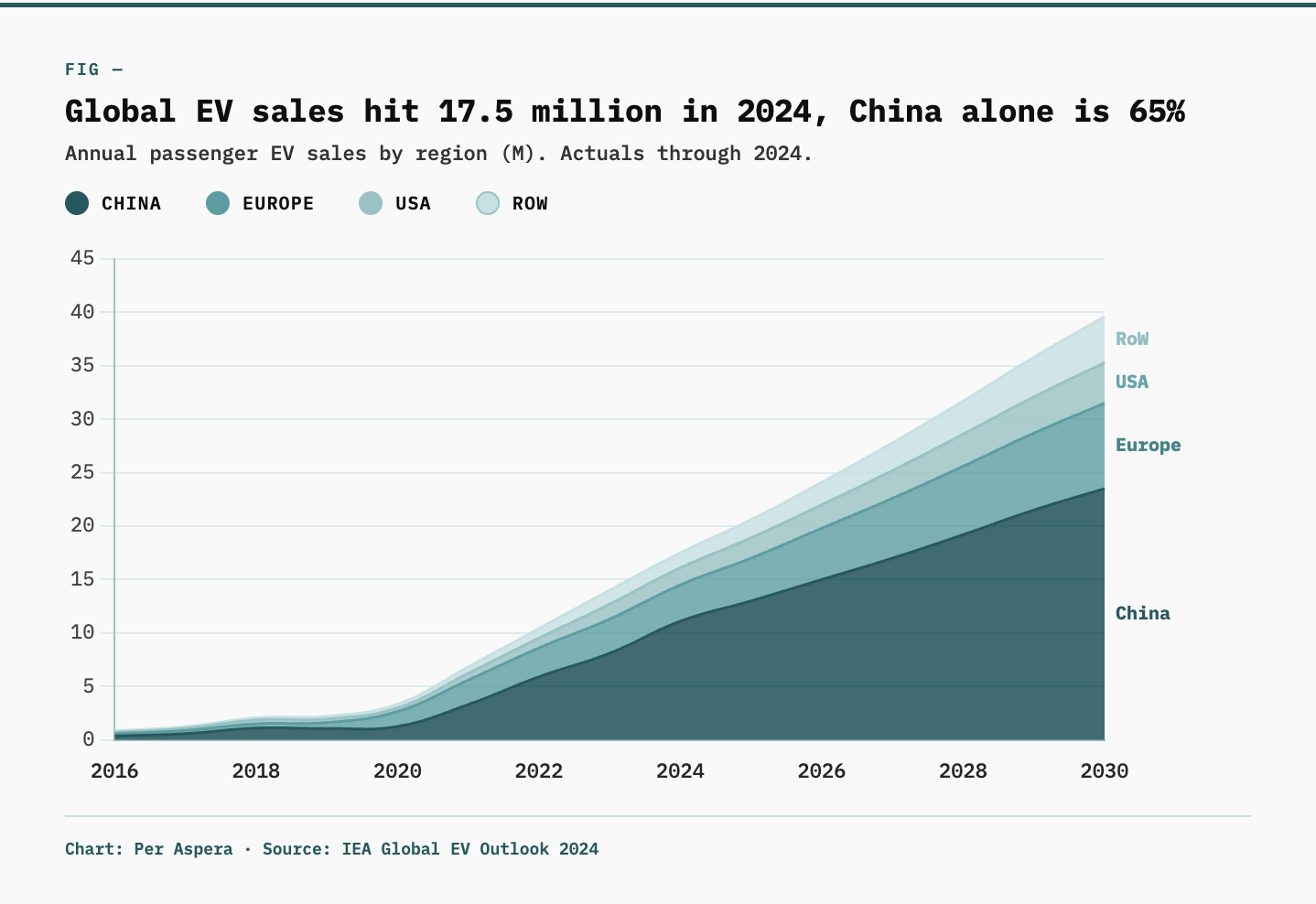

Nearly all battery‑grade graphite is made in China, and U.S. demand is set to ~5x by 2030. As today’s guest tells us, China controls the battery-grade graphite production, the downstream knowhow, the underlying equipment, and the “equipment to make the equipment.” This is a textbook case of what we here at Per Aspera like to call Strategic Amnesia: as the West willingly outsourced capacity to produce this commodity, we also regulated, offshored, and culturally disowned the relevant chemistry, and in the process, we forgot how to do the thing.

Molten’s answer is ambitious, but intuitive: start with something America has in abundance – cheap natural gas. Through process innovation on methane pyrolysis, turn that into battery-grade graphite, with a valuable industrial byproduct: hydrogen (!). This avoids the ugly parts of conventional approaches, making it a more palatable approach in the U.S.

Company at a glance

- Co-founders: Caleb Boyd and Kevin Bush, both Stanford materials-science PhDs in thin-film solar.

- Process: Methane pyrolysis. Natural gas in, graphite and hydrogen out. No oxygen, no toxic post-processing.

- Pilot: A reactor in Oakland producing three tons of graphite and one ton of hydrogen per day.

- First commercial plant: TBA “soon,” pending final siting and state incentive negotiations.

- Five-year roadmap: Facilities in the high hundreds of megawatts producing hundreds of thousands of tons of graphite and hydrogen per year by 2030.

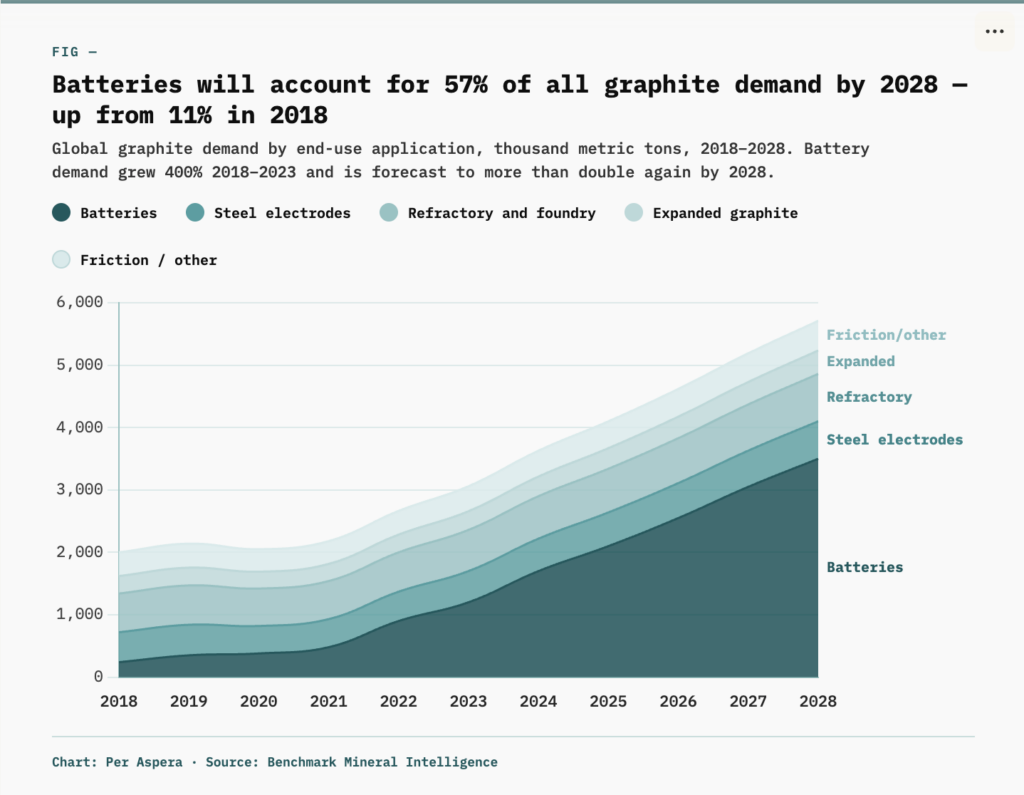

- Market context: US lithium-ion battery demand for graphite is roughly 200,000 tons today, on a path to 1M tons by 2030.

We’re excited to present episode 1 of Hard Reflections, a new storytelling series from Per Aspera, with Caleb Boyd, cofounder of Molten Industries.

Why are we starting with Caleb? Because he’s a longtime member of our community and an avid reader of Per Aspera, with the added, serendipitous small-world weirdness of having bumped into Crusey during his VC days while looking at space deals. He got on our radar the best way possible: by writing in after we mentioned precursor bottlenecks March edition and put out a call for American chemists to get in touch. That is the community-driven flywheel we’re all about cultivating here: serious readers, close to the problem and engaged in important, hard pursuits, volunteering to turn themselves into contributors, collaborators, sources of tribal knowledge, narrators of industry war stories, and occasional well-informed nuisances in our inbox (not that Caleb falls into that last category, but if you want to play this role, bring it on and sound off).

He wrote in volunteering his chemical insights, dual-hat experience (as founder and reformed VC), and ambitions to build America’s next Dow Chemical. And of course he got our attention when he said:

Ninety-nine percent of the graphite for lithium-ion batteries today is made in China. I'd argue it is the single largest dependency across US defense and our daily lives, and massively overlooked.

So we (the triple threat of Dan, Ryan, and Joy) got Caleb on the horn. What followed was a wide-ranging chat on graphite, methane pyrolysis, China, batteries, industrial chemistry, permitting, power, and what happens when two Stanford PhDs start tinkering in a garage during the pandemic, trying to make the cheapest hydrogen on the planet, thinking they’ve accidentally figured out a way to create diamonds, and ultimately discovering something rarer…

Please enjoy this conversation with Caleb Boyd of Molten Industries, which has been edited for clarity and length. (And if you’d like to get involved, read to the bottom for notes on how to do so.)

The Interview

Ryan Duffy: What’s the elevator pitch you give to investors, potential hires, or other strategic audiences for how the United States found itself in this supply-chain situation? For graphite specifically.

The process for synthetic graphite production was invented in the USA by Edward Acheson in 1890. I’ve got a batch of some of the original Acheson Graphite on my desk as a reminder to the days when America led the graphite industry. Since then, as-is with so many other critical minerals stories, we’ve ceded massive ground by choosing to under-invest in manufacturing supply chains and purposefully pushing out chemical and minerals manufacturing that is often messy and distasteful to the “Not In My Backyard” types.

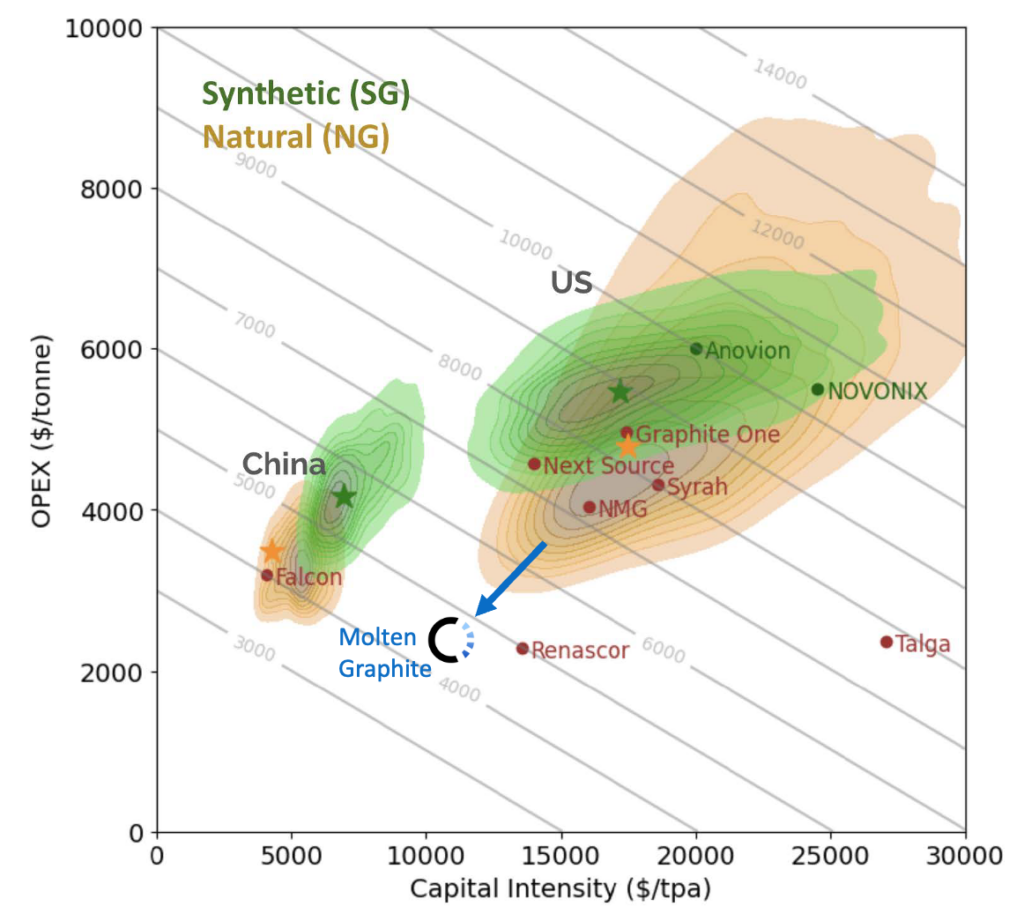

There’s a handful of mining and artificial-graphite companies trying to make it work in North America. They’re either mining natural flake graphite, which has its own environmental intensity and mostly happens in China anyway, or they’re running the Acheson artificial route — heating petroleum coke to something like three thousand degrees Celsius, roughly half the surface temperature of the sun. But copying what is done in China today in the USA is simply not going to be competitive..

Dan Goldin: What we’re trying to do here is find who’s at the bleeding edge, who has really done the hard stuff, and why we should care. So I’ll start a little sharply. There was just an article in the Wall Street Journalabout how all the business is drying up to EV suppliers because of drill baby drill. I know I’m a little difficult — but come at me.

Drill baby drill fits exactly into our thesis at Molten. We take natural gas, heat it to high temperatures, and split it into graphite and hydrogen. The graphite can be used for all sorts of things; the largest growing market right now is lithium-ion batteries. What’s unique about what we do is that we’re the only company in the world that can take natural gas and turn it into battery-grade graphite at scale. So when you talk about drill baby drill versus EVs, Molten is actually using drill baby drill to make more EVs and stationary energy storage systems.

Joy Shin: What’s driving the demand?

One: stationary storage paired with wind and solar is going into the buildout of every major industrial and commercial asset, including datacenters. There’s a narrative right now that datacenters run on gas — and yes, we’re using drill baby drill to make graphite — but a lot of new datacenters will use stationary storage too.

Two: autonomous-vehicle fleets make sense as EVs because total cost of ownership matters more the more you drive, and AV fleets are going to take off over the next five years.

Robots and drones are the third wave that have yet to create massive demand but are coming in the 2030s. All of those things require batteries, and all of those batteries require graphite.

But graphite goes beyond batteries. It’s used in nuclear reactors (both fission and fusion reactors), it’s used in the Czochralski furnaces to make silicon ingots for computer chips and solar cells, and it’s used in rocket nozzles and thrusters.

The future is built on graphite.

Dan Goldin: I’ve done a lot of work around data centers, and the economics are brutal: dollars per cubic centimeter, dollars per kilowatt, dollars per kilowatt-hour. That is why I’m pressing on cost. You have all these wonderful things, and you use gas. Come to confession.

The EV and storage markets are going to keep growing because cost matters more as utilization rises. Stationary storage is becoming part of the buildout of major industrial and commercial assets, including datacenters.

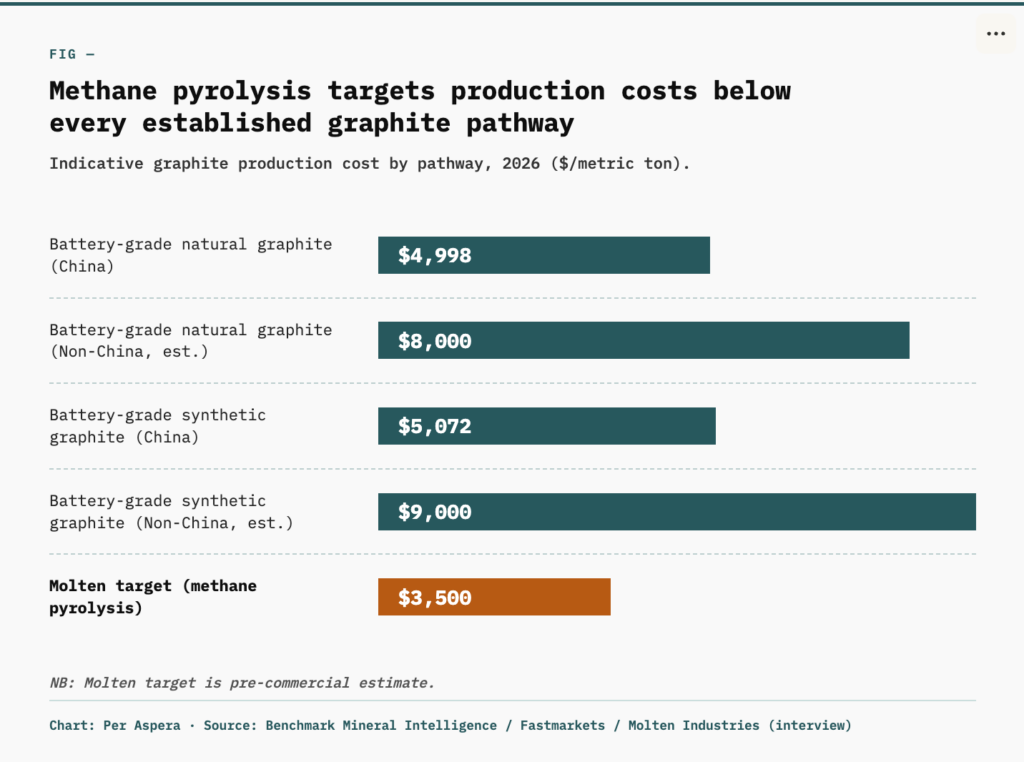

And AV fleets are going to be EVs, because the more you drive a car, the more electric powertrains make sense for total cost of ownership. So $/kwh will absolutely be the metric every manufacturer is going to dominate on. By using natural gas, and by being the only company in the world that can use natural gas to make graphite for batteries, we’re able to produce the lowest-cost graphite globally.

Dan Goldin: By the way, if I were putting up a plant I wouldn’t put it in California. I’d go to North Dakota — from the space station they could see the gas emissions and they’d love to put them to good use.

In the near term, we can produce the lowest-cost graphite in the United States from our first plant. That plant is not going to be in California. You can imagine the state where it might be but I won’t announce it just yet.

The combination of low-cost natural gas, low-cost electricity, and the ability to build means we’ll undercut every other graphite producer in North America or Europe. Our second and third plants directly compete with China. And when we start unlocking really low-cost gas resources — flare sites in North Dakota, stranded gas in Argentina or Qatar — this becomes the lowest-cost pathway to produce graphite globally.

We’ll be making graphite, and exporting it to China! . China is going to continue to be the 80% market leader in batteries through the next decade. That’s a core part of our thesis: North America first, but China is still core to the long-term.

Think of this like LNG. Upgrade low-cost natural gas into graphite, and then ship it globally to be used anywhere where graphite is in demand.

Ryan Duffy: What’s the origin story for you guys? How has the thesis evolved since you founded the company?

Kevin [Bush, CEO and cofounder of Molten] and I both did our materials PhDs at Stanford in thin-film solar. He went and worked at another solar startup, then founded one, and I went into VC. During the pandemic we got back together and started tinkering in a garage on Stanford’s campus, where Kevin was living. We built an electrical-resistive heater off his landlord’s EV charger, sourced methane from a local gas-supply store, and started splitting methane into carbon and hydrogen. The original thesis was hydrogen: how can we produce the lowest-cost hydrogen in the world? Methane pyrolysis is interesting because you use way less electricity than something like water electrolysis, and you produce two valuable products — a carbon product and a hydrogen product.

So we did that on the side for about a year and a half, and partway through, we started making high-quality graphite. When we initially made it, Kevin actually thought it was diamond — we got really excited. Synthetic diamond does come out of methane pyrolysis under different conditions, just at higher cost.

That changed the entire trajectory. Molten became a graphite company with a hydrogen byproduct, instead of a hydrogen company with a carbon byproduct.

Dan Goldin: You don’t do diamonds with this process, but you could do graphene. Could you say a few more words about the graphene byproduct?

We didn’t invent methane pyrolysis. There are a couple dozen methane-pyrolysis companies globally — Monolith Materials in Nebraska makes carbon black for tires; others use plasma to make graphene-type carbons. The difficulty is several-fold. One: methane pyrolysis creates a carbon product that clogs up reactors the way cholesterol clogs an artery. We developed a way to prevent that. Two: making a graphite product that’s actually usable for a large downstream market is hard. And graphene is harder still — there’s no one-size-fits-all graphene. The graphene that wins Nobel Prizes needs to be highly oriented, flat, large-domain. That’s hard out of any process. Companies haven’t figured out how to do it economically and at scale.

We could make graphene from our flake. The original way graphene was invented was scotch tape on graphite — pulling layers apart. You can do it chemically at scale by putting flake into a tank reactor with the right reagents. But we don’t see downstream demand worth pursuing right now.

At a startup, focus is the advantage. The focus right now is low-dollar-per-kilowatt-hour battery-grade graphite. [Editor’s note: This is a key tenet of Faster Better Cheaper – “Reduce Programs and Products to Single, Simple Metrics” – so we’re in agreement with Caleb here]

Ryan Duffy: What has the journey been like? From what I can see externally, you’re pretty far along and relatively low-profile. Are you trying to fly under the radar?

We’re going to make a switch to being a much more publicly focused entity shortly. Everything to date has been very under the radar. We’re not in stealth mode — that’s a little overblown — but there’s an advantage in sharing as little as possible.

Joy Shin: What’s the difference between natural and synthetic graphite? Why does it matter?

You mine natural graphite out of the ground. It’s essentially the rare-earths problem: to get to high-quality natural graphite, you need processing that’s environmentally intensive. You have all this rock embedded in the graphite that you have to leach out with acids. That was pushed to China for environmental and cost reasons, like the classic rare-earth-processing story.

Synthetic graphite is made from petroleum coke — the bottom of the barrel of refinery output. You take it and heat it to 3,000°C. That was invented by an American — Edward Goodrich Acheson — in the late 1800s, and it’s been done in the U.S. ever since. You literally dig a pit in the ground, put coke blocks into the pit between two electrodes, bury them in carbon dust, and run high current through. The blocks heat up to half the surface temperature of the sun. The carbon dust prevents them from burning away. That process is incredibly energy-intensive — and to Dan’s earlier point, energy price matters a lot — and it emits sulfur oxides, nitrogen oxides; anything that’s not carbon vaporizes away in the pit.

For similar reasons, a lot of that has moved to China and other countries. The US is waking up to the realization that some of those decisions — things we don’t want to do here because they don’t necessarily look nice or feel nice but are necessary — have real downstream implications.

You reap what you sow when, for decades, you say: avoid this list of things at all costs.

Ryan Duffy: We noted a couple months ago that the chemical industry is really struggling in Europe. Have you tracked that?

Exactly. Europe just released a proposed ruling on a list of critical chemicals they need to maintain production of. That list is the list of all the things everyone has been saying for the last decade — multiple decades — that you don’t want on an industrial site: benzene, toluene, hydrofluoric acid. Usually you see those lists on the places you don’t want to go. You don’t want to put it into your chemical plant, because you’re going to get into a lot of trouble. Now the EU is saying: ‘these are critical chemicals and we need to maintain production.’

You reap what you sow when, for decades, you say: ‘avoid this list of things at all costs.’ People will learn to avoid them. You’re going to push them out of the country.

Ryan Duffy: In terms of human capital, or what we like to call tribal knowledge, Dan probably has thoughts here too — how would you characterize the state of materials-science training and the workforce in the United States?

The US has some amazing material scientists and amazing lab research. But the tribal knowledge in specific areas has left the U.S. – perfect example, graphite. China has 99% of global battery-grade graphite production. The entire supply chain — all the knowhow of how to make graphite that’s good for batteries, that you’re putting into a stationary energy storage system, drone, robot, or EV — and the equipment to make it, and the equipment to make the equipment — is all concentrated in China.

That’s incredibly important for the US to realize. Our approach at Molten is that we’re going to need to partner with China to make US-made graphite again. Reinventing the wheel isn’t necessary — we’re reinventing the way the core graphite block is made. The downstream processing for that block before you put it into a battery, all that knowhow is in China.

North America first in the short term, global leader in graphite production in the long term — which means China is part of the long-term strategy. Finding ways to partner there is important. It’s not true for DoD-adjacent companies, obviously. But for companies in the energy and materials space, finding bridges we can maintain matters.

Dan Goldin: How are you going to protect your technology against China espionage and stealing? They’re awful. I’ve been dealing with this problem for decades.

Caleb Boyd: We’re incredibly careful about where we partner. For our core methane-pyrolysis technology, we do all the machining of our systems and all the manufacturing of our systems entirely in-house.

Dan Goldin: Do you have any market in the US to make lithium-ion batteries — graphite to American manufacturers of lithium-ion batteries?

About 200 gigawatt-hours — 200,000 tons — of graphite is used for lithium-ion batteries in the US today. That will grow to about a terawatt-hour by 2030. A million tons of graphite. The majority of that goes to gigafactories: Tesla, Panasonic, Samsung, LG Energy Solution, SK, etc. Our goal is to initially win the US graphite market and then expand from there globally.

Joy Shin: Who are your materials-science heroes? What about them do you admire?

I’d say chemistry heroes more than materials-science specifically. The Haber-Bosch process is incredible. It feeds the eight billion people on this planet — using hydrogen to fixate nitrogen from the air, creating ammonia.

What I admire is the combination — Haber’s scientific greatness, achieving something in the laboratory that no one thought was possible, combined with Bosch’s ability to take that and run it to scale by beating on it from an industrial standpoint. That combination is what’s beautiful about that story. You don’t see it often. A lot of times you can achieve something amazing in the lab and you never get it to scale. That’s the story of where the US has had difficulty over the last decade — we’re good at scaling things, but we’ve had difficulty coming up with the insane breakthrough inventions in the lab.

Joy Shin: From where you sit, as a former VC and now as a founder, what do you think are the things we can do to help transition from R&D to scaling more aggressively?

A lot of what this administration is doing in terms of deleting constraints and barriers to scaling. Make building, permitting, facilities, industrial plants, energy as easy and as quick as possible.

When you’re a startup, you have a finite lifespan. If half of that is consumed by 18 months, or multiple years, of waiting for permits and regulatory review, that’s a death blow to scaling new technology. The speed there really, really matters.

At a macro level, incentives or protectionary measures for US companies entering global commodities markets cuts both ways. It’s good if you’re making that commodity, but bad if you’re buying it. What came out in OBBBA around battery and stationary-storage tax credits, and the requirement to source batteries from US or non-FEOC sources, has created a huge demand for North American graphite at a price point dislocated from global supply. That helps us in the near term. But there are also things that don’t help us — we’ve paid a bunch of tariffs in the near term too.

Dan Goldin: Cost per unit is critical. And power is a victim product as I like to say. It’s exposed to the Strait of Hormuz, a victim of competition between industry and homes on the grid, and to energy markets more broadly. If you can secure your own energy source over time, you decouple from the system. You’re in control. You can project out your costs. That’s a real positive asset, especially when you get big. Does that make sense to you?

I agree. For our first plant, we’re going to be a mix of renewables and grid power because we need backup availability. Moving forward, we certainly see decoupling as an asset.

Ryan Duffy: Can you say anything about the power intensity of your facility?

The first plant we’re targeting is a 20-megawatt power hookup. That’s small relative to the gigawatt data-center hookups that are getting put on these days.

In our five-year roadmap, we want to be making facilities producing hundreds of thousands of tons per year of graphite and hydrogen — those will be in the high hundreds of megawatts of power requirements.

Ryan Duffy: What’s the critical path for Molten in the next six to 12 months? I know you’ve flown relatively under the radar but what can you talk about?

Standing up the next facility, in the tens-of-thousands-of-tons-per-year range for graphite and hydrogen. This is what I’d call commercial scale, but it’s still small for world scale.

From there, we want to scale as quickly as possible to world scale, which means hundreds of thousands of tons per year of graphite and hydrogen by 2030. Getting to that scale as quickly as possible is what battery companies are looking for. They’re currently desperate for North American supplies of battery materials, and the downstream users are right behind them.

Dan Goldin: Graphite is pretty good at high temperatures, isn’t it? One of the principal problems limiting hypersonic aircraft is the ability to withstand high temperatures. As a materials expert, what do you think about the solutions?

Graphite is used in nose-cones and tail-cones of rockets, and used in nuclear reactors.

Dan Goldin: Ten years from now, how do you visualize Molten Industries? Pick five years, ten years, twenty years, whatever it is. What’s your vision? Second: how do you scale it?

On vision, what I’d say is that Molten in ten to twenty years is a generational materials and chemical manufacturing company. Graphite for batteries is the tip of the spear. We become the lowest-cost graphite producer globally. As you scale that, you get a Jevons-paradox effect — graphite is used to make silicon, by the way, in graphite crucibles — so as graphite gets cheaper, you start using it for thermal-energy storage, structural materials where temperature matters, all sorts of new use cases. And our hydrogen byproduct plays a big role: hydrogen is the baseline for ammonia fertilizer, methanol, synthetic fuels. We become a fuels and chemicals producer using that byproduct stream.

On scaling, this is something China does very well. And Elon approaches it very well at SpaceX. It’s a core value at Molten: don’t let perfect be the enemy of the good, and don’t over-optimize your system. Build the minimum viable system to make something economically, then multiply or scale that as quickly as possible. Elon talks about this with the hydrogen-versus-kerosene approach. Kerosene gets you 80% of the efficiency of hydrogen at a fraction of the cost, and the system-level economics are dramatic.

We’re scaling in a modular fashion. We have a single unit here in Oakland today where we’re headquartered doing one ton a day of hydrogen and three tons a day of graphite. We’re going to multiply that unit for our first plant.

Is that the theoretically perfect maximum-efficiency layout? No. Does it let us move as quickly as possible and hit economies of scale faster? Yes.

Ryan Duffy: Perhaps there’s a historical analogue here?

The analog is Dow Chemical. Dow started by extracting bromine from brine in the Midwest, when German bromine companies held complete dominance and tried to strangle the new entrant. Dow’s process was simply better. Today nobody thinks of Dow as a bromine company — they make everything.

Joy Shin: One last question. A big part of this series is learning from the community. What can we be doing, and the broader reindustrialization movement, be doing better for the chemical sector?

I’ve been super excited about the reindustrialization movement over the last couple of years. I love what you all are doing at Per Aspera. You’re showing how these bottlenecks connect — from raw materials and chemistry to factories, batteries, energy systems, and the end markets that depend on them. It’s incredible. Keep shining a light there. It’s working.

Want to get involved?

Hard Reflections exist to surface the people behind people behind the companies, movements, and ideas building the hard parts of our future: materials, machines, energy systems, factories, infrastructure, space, defense, semiconductors, chemicals, and the physical stack underneath AI. If you are a founder, physicist, engineer, chemist, operator, investor, program manager, or unusually obsessive domain expert working in one of those arenas, we want to hear from you.

The best way to get on our radar is not to pitch us cold, so we won’t provide a form. Rather: read Per Aspera. Subscribe if you haven’t already. Spend time with the back catalog. Then reply to something we’ve said (or say in a forthcoming edition) that maps to your hard pursuit, tribal knowledge, or your earned hot take. Tell us what we missed, what we got right, why there’s a better way, what everyone’s missing, and how some combination of these things informs what you’re working on, whether it’s a company you’re building, thesis you’re funding, the object of your research/academic obsession, or the philosophy against which you operate. You can nominate yourself or someone else.

Humongo bonus points will be awarded if your submission starts where Caleb’s did: by highlighting a big problem hiding in plain sight, and how you’ve made it your life’s work to solve it.

Caleb Boyd is Co-founder of Molten Industries.

Ryan Duffy is Editor in Chief of Per Aspera.

Dan Goldin is our own Honcho of Per Aspera.

Joyce Shin is a Co-founder of Per Aspera.